United States President Biden has recently commented: “But let me be very clear: Capitalism without competition isn’t capitalism; it’s exploitation. Without healthy competition, big players can change and charge whatever they want and treat you however they want. […] So, we know we’ve got a problem — a major problem.”

It’s not every day you hear the President of the United States take on the very industry that supported his national economy remaining the world’s richest over the past couple of decades. Yet his tone resonates with a growing unease within the US and elsewhere over the extraordinary rise of these technology giants, not just in monetary terms but in terms of their social power as well. He is reflecting a growing sentiment that the current situation looks like it will never be adequately corrected by just competitive pressures within market itself. Some further forms of regulatory intervention will be needed to force a fundamental realignment of these players. In so doing, it appears that regulators appear to be finally catching up with the online world in the US, in Europe and in China. I’d like to explore this topic here.

Anti-Trust Legislation

However, first some background to this topic.

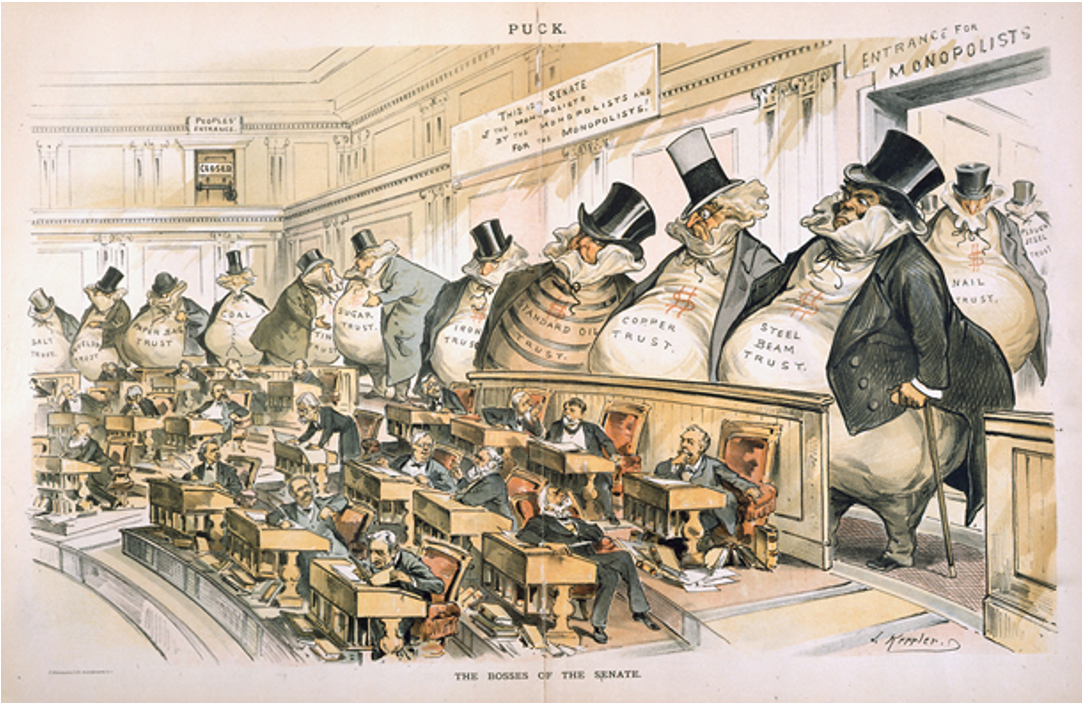

The Sherman Antitrust Act of 1890 was a US Federal measure intended to curb the emerging power of corporate trusts. It was named for Senator John Sherman of Ohio, who was a chairman of the Senate Finance Committee and the Secretary of the Treasury under President Hayes. Several states had passed similar laws, but they were limited to intrastate businesses. The Sherman Antitrust Act used the constitutional power of Congress to regulate interstate commerce. The Act passed through the Senate and Congress with overwhelming support on the floor and signed into law on 2 July 1890, by President Harrison.

A “trust” was an arrangement by which stockholders in several companies transferred their shares to a single set of trustees. In exchange, the stockholders received a certificate entitling them to a specified share of the consolidated earnings of the jointly managed companies. The trusts came to dominate a number of major industries, destroying all forms of competition in the process. For example, on January 2, 1882, the Standard Oil Trust was formed. A Board of Trustees was set up, and all the Standard Oil properties were placed in its hands. Every stockholder received 20 trust certificates for each share of Standard Oil stock. All the profits of the component companies were sent to the nine trustees, who determined the dividends to be distributed to the certificate holders. The nine trustees elected the directors and officers of all the component companies. This allowed the Standard Oil to function as a monopoly since the nine trustees ran all the component companies. The Sherman Act authorized the Federal Government to institute proceedings against trusts in order to dissolve them. Any combination “in the form of trust or otherwise that was in restraint of trade or commerce among the several states, or with foreign nations” was declared illegal.

A “trust” was an arrangement by which stockholders in several companies transferred their shares to a single set of trustees. In exchange, the stockholders received a certificate entitling them to a specified share of the consolidated earnings of the jointly managed companies. The trusts came to dominate a number of major industries, destroying all forms of competition in the process. For example, on January 2, 1882, the Standard Oil Trust was formed. A Board of Trustees was set up, and all the Standard Oil properties were placed in its hands. Every stockholder received 20 trust certificates for each share of Standard Oil stock. All the profits of the component companies were sent to the nine trustees, who determined the dividends to be distributed to the certificate holders. The nine trustees elected the directors and officers of all the component companies. This allowed the Standard Oil to function as a monopoly since the nine trustees ran all the component companies. The Sherman Act authorized the Federal Government to institute proceedings against trusts in order to dissolve them. Any combination “in the form of trust or otherwise that was in restraint of trade or commerce among the several states, or with foreign nations” was declared illegal.

The US Federal sector made extensive use of the Sherman Act in the period 1890 – 1915. President Theodore Roosevelt sued 45 trust companies under this act, while William Howard Taft sued a further 75 trusts. There were a number of high-profile actions under the Sherman Act, including the divestitures of Standard Oil, American Tobacco, and General Electric, all in 1911. However, the appetite to continue to apply this legal provision waned in the ensuing years. There were probably a number of factors behind this. The break-up of these large enterprises caused some consequent ripples through the national economy and played a role in the US economic panic of 1911. Congress established the Federal Trade Commission (FTC) in 1914, whose legal and business experts could force business to agree to “consent decrees”, which provided an alternative mechanism to police antitrust. At the same time the most egregious labour-exploitative business practices of large corporations was moderated by “welfare capitalism” in the 1920’s. For example, the Ford Motor Company dominated global auto manufacturing, built millions of cheap cars that put America on wheels, and at the same time lowered prices, raised wages, and promoted manufacturing efficiency. This emergence of US dominance in international markets for manufactured goods meant that the US domestic economy was a major beneficiary of such large-scale US enterprises dominating the global market, making them politically untouchable in the domestic context. Subsequently, such dominant enterprises turned to political lobbying to forestall political action in the form of anti-trust actions. Consequently, these anti-trust provisions were largely unused through most of the 20th century and were only brushed off again in the action bought against AT&T in 1982.

The Rise of the Digital Giants

It was this action against AT&T that was one of the triggers for the explosion of the Internet around a decade later. AT&T had largely suppressed the rise of data communications through prohibitive tariffs for its services and an aversion to invest in packets network research at the time. It saw data networks as a wedge that would ultimately threaten its monopoly in communications services, and it left the field open for DARPA to explore using federal funding. The divestiture of AT&T created a collection of rapacious “Baby Bell” enterprises who were successful in arguing for the deregulation of the telecommunications market. At the same time computers were leaping the gap from expensive specialised instruments to consumer goods with the introduction of the personal computer, and there was a happy co-incidence of demand and supply that fuelled the transformation of the telecommunications sector. The result was as explosive as the great railway mania of the 1840’s in the United Kingdom, or the rapid economic and industrial growth of the Gilded Age in the US in the 1880’s. Microsoft was an early leader in the personal computer market, but it was Cisco that was an early darling of the Internet with an initial public offering in early 1990 that produced an instant market capitalisation of $224 million. It may sound like a minor sum today, but at the time it was an attention-grabbing fortune! And the dot-com bubble was born.

The bursting of the dot-com bubble in 2000 cleared away much of the initial hysteria over the Internet, and in its wake, we saw a second wave of digital entrepreneurism that subsequently overtook the peaks of the dot-com bubble and continued with an inexorable rise to not only dominate but define the global digital space. We all know these names, as they are simply part of pretty much everyone’s life these days: Apple, Microsoft, Amazon, Alphabet (Google), Facebook, Tencent and Alibaba. Apple and Microsoft now have a market capitalisation in excess of 2 trillion dollars, Amazon and Alphabet are both at around 1.7 trillion dollars and Facebook at just under 1 trillion.

The digital world is now totally dominated by these big seven corporates, and there are some rather troubling issues emerging. The economic model that these enterprises are using these days goes by the name of “surveillance capitalism” where the data associated with each customer’s individual interaction with the service is collected, analysed, and then used to feed profiling models that are used to guide the service’s subsequent interaction with that customer. This includes ad placement, but may also involve search result tuning, navigational guidance, or similar customised service responses. The erosion of our expectations of personal privacy is a rather disturbing by-product of this unprecedented concentration of attention on the customer, but there are a number of more common undesired outcomes as well, including the elimination of competition, the active suppression of disruptive innovation from any third party, and the clear formation of cartel-like behaviour from these major market actors.

In many ways this is a repeat of the situation that emerged in the Gilded Age in the US in the 1880’s where the leading market actors were moving far faster than the ability of public institutions and the legislators to react. What it meant was that these entities were out on their own with their unique operational business model and they were able to define their own terms of interaction with customers, with their labour force, with each other and with the public institutions of the day.

This has happened again with the digital enterprise models used on the Internet, and it has taken the public sector more than two decades to catch up with these extremely nimble enterprises. It should be stressed that this is no longer a telecommunications policy issue. We have moved well beyond telecommunications here and we find ourselves in the domain of commerce and enterprise, where the medium and environment is defined by the behaviour of the applications running on our devices. When we talk about how to regulate the actions of Facebook, we are not all that far from the hypothetical conversation on how to regulate the actions of applications such as Word or Excel! What we are in fact talking about is the behaviour of these digital services and they ways in which we interact with them.

This has happened again with the digital enterprise models used on the Internet, and it has taken the public sector more than two decades to catch up with these extremely nimble enterprises. It should be stressed that this is no longer a telecommunications policy issue. We have moved well beyond telecommunications here and we find ourselves in the domain of commerce and enterprise, where the medium and environment is defined by the behaviour of the applications running on our devices. When we talk about how to regulate the actions of Facebook, we are not all that far from the hypothetical conversation on how to regulate the actions of applications such as Word or Excel! What we are in fact talking about is the behaviour of these digital services and they ways in which we interact with them.

So, what are we doing about it?

There is legislation being drafted that is aimed at curbing the power and influence of the big technology companies in both the United States and Europe, while in China, the government has already implemented sweeping changes to the way Chinese technology companies can operate both in China and beyond.

The US efforts

There is a visible preference in the United States for using the courts to curb the power of these digital giants, and this is reflected in a number of legal decisions in recent times. A good example is a recent ruling by a federal judge in California that Apple must allow app developers to steer users to payment options outside Apple’s App Store and thereby avoid the fees (to up to 30%) levied by Apple. This is a move that is likely to be visible in the corporate giant’s financial bottom line as Apple is increasingly reliant on its e-commerce margins rather than rely solely on platform sales. Behind these legal actions is a number of proposed legislative actions intended to strengthen the legal framework to curb the overwhelmingly dominant market position of the current behemoth incumbents.

There are five bills before the US legislators, following a 16-month investigation by the House Judiciary Committee. The measures are headed for a house vote, preceding a Senate vote and then Presidential assent. There is a lot of opportunity to derail this process, but the fact that this has got this far already reflects a sense of unease that these tech giants have been perceived to be abusing the massive social reach and commercial powers, gaining overwhelming relative market power over potential competitors, or simply purchasing competitive technologies with a view to either integrating it into their product or simply suppressing its further development. This Congress appears to be serious about this topic and is attempting to move forwards with a legislative agenda on a bipartisan basis.

The “Ending Platform Monopolies Act” makes it illegal for a platform operator to bias outcomes and selection of services in favour of other companies that they own. The legislation is saying in effect that “you can be a marketplace or be a seller of goods, but you really can’t be both at once” This has attracted the most opposition in Congress at present. It would force a breakup of the corporate “umbrella” where individual companies hand off users to other companies in the same corporate group in preference to any third-party provided service. It appears to target Amazon and Apple in particular, as its provisions are limited to retail sales companies that have a market capitalisation larger than $600 billion, which is of course a highly selective filter.

The “America Choice and Innovation Online Act” would prevent companies from using data that they obtain by being a platform. For example, it would prevent Amazon using their platform data to support selling their own party products on an unfair competitive basis with products from third parties. It would also prohibit other types of discriminatory behaviour by dominant platforms, such as cutting off a competitor that uses the platform from the services offered by the platform. It also prevents dominant platforms from using data collected on their services that isn’t made available to other platform suppliers to fuel their own competing products.

The “Merger Filing Fee Modernisation Act” is a bipartisan bill that is intended to revive effective antitrust enforcement in the United States. The bill proposes to increase enforcement resources for the Federal Trade Commission and the Antitrust Division of the U.S. Department of Justice by more than $154 million, or almost 30 percent. It would also adjust the merger filing fees system so that fees would more equitably fall on larger deals. The bill alone will not solve the market power problem in the U.S. economy but increasing the enforcers’ capacity to bring more cases is a necessary first step. Currently, the merger fee for transactions of entities where the merger transaction is in excess of USD $919M is USD $280,000. The proposed bill changes this filing fee to $2.25M for transactions of $5B or more. It seems to me that the impost on mergers and acquisitions has risen from a risibly minute level to something that is still laughably insignificant. If this is the best indication that the US Congress can give to signal that is it focussed on the issue of mergers and acquisitions as an anti-competitive tool then frankly its reasonable to conclude that this level of Congressional focus falls somewhere close to woefully too little and lamentably ineffectual!

The “Platform Competition and Opportunity Act” is proposed to shift the burden of proof in merger cases to dominant platforms to prove that their acquisitions are in fact lawful in terms of not impairing levels of competition, rather than the regulator having to prove the acquisition will lessen competition. This measure would likely substantially slow down acquisitions by dominant tech firms.

The “Augmenting Compatibility and Competition by Enabling Service Switching (ACCESS) Act” would mandate dominant platforms maintain certain minimum standards of data portability and interoperability regarding the data they collect and store about consumers, making it easier for consumers to take their data with them to other platforms, and also pushing industry-wide use of common data formats and interchange between these platforms. It strikes me as a distinct risk of this bill in enacted that it would take a small set of distinct platforms and create a single cartel. Such an outcome would probably be somewhat worse in terms of entrenched barriers to competition than today’s situation.

These bills would be significant if they pass through the legislative process unscathed, and unsurprisingly the tech giants have been lobbying intensively to try and ensure that Congress will not pass these bills in their current form.

The EU

There are 2 draft bills before the EU Parliament, the Digital Services Act, and the Digital Market Act. Like GDPR measures that preceded it, these are both potentially significant pieces of legislation.

The Digital Services Act puts more responsibility on the part of service providers, and it is intended to highlight their responsibility in taking an active role in content moderation decisions. It also directs them to make such decisions more transparent and appealable.

The Digital Markets Act will moderate the speed at which digital enterprises can effectively “take over” markets. It’s a significant piece of legislation by changing the regulator’s toolset by forestalling planned corporate acts rather than reacting after the event and trying to mitigate the consequence. As with the previous GDPR measures, fines are significant at up to 10% of global revenue for the corporation. These potentially massive fines have attracted headlines, but it’s clear that the fines are less of an issue than the measures to forestall private sector actions and require corporate actors to engage the regulator beforehand.

The EU legislative process is tortuous and somewhat opaque at times so there is much to happen in the next 18 months as these measures wind their way through the process.

Meanwhile, France and Germany are both impatient to see change and are acting unilaterally as a lead to potential EU action. Germany has already made a change at the start of 2021 so that large scale platforms, including Amazon, can be pre-emptively shut out from a suite of actions within the German market. The French action continues a well-established pattern of requiring social platforms to have active moderation of content, particularly relating to hate speech. Both countries are trying to influence the broader EU response in whatever the final EU-wide rules may be.

The Digital Markets Act appears to be a continuation of the line of through put forward by Luis Brandeis in the US in the first part of the twentieth century, when he argued that big business was too big to be managed effectively through post-facto regulatory actions in all cases. He noted that the growth of such very large enterprises that were at the extreme end of the excesses of monopolies, and their behaviours harmed competition, harmed customers, and harmed further innovation, while at the same time the quality of their products tended to decline, and the prices of their products tended to rise once they had achieved market dominance. When large companies can shape their regulatory environment, take advantage of lax regulatory oversight to take on more risk than they can manage, and transfer downside losses onto the taxpayer, then we should be very concerned, as the public sector would by then have lost its power to respond to such destructive and exploitative corporate practices by these monopolists. He was in effect arguing for pre-emptive curbs on emerging monopolies and market distortions, in line with the current provisions in the Digital Markets Act.

China

There is a sense of catching up in China to introduce consumer protection measures that have been a feature in European and Norther American markets for years. There are, however, some basic differences between China and the US and Europe.

The US and European situations are moderated by the activity of industry lobbyists, where the case for curbs and controls is moderated by the case that such enterprises are powerful generators of wealth in post-industrial societies. China’s response is far more along the lines of direct intervention in the market.

Shares in Alibaba have fallen sharply following reports that Chinese regulators want to break up Ant Group, the huge financial-technology firm affiliated with Alibaba. The Financial Times has reported that Ant will be directed to divest Alipay, the world’s largest payments platform, and hand over users’ data. Alibaba’s outspoken co-founder, Jack Ma, has reportedly fallen out of favour with the Chinese Communist Party.

The restrictions imposed by Beijing in recent times includes ride hailing services, social platforms and ecommerce, online education These are not subtle changes in the overall environment but quite explicit measures. A little over a year ago Jack Ma made some less than complementary observations about the ruling leadership in China and their ability to drive a policy agenda that was effective in the broader context of an increasingly sophisticated national digital agenda. He was swiftly bought into line by the national leadership, who then triggered a set of changes that have taken on a far wider agenda. It’s not just about regulating Big Tech entities in China, and it goes into the entire notion of the makeup of Chinese society. The emergence of a monied elite is seen to be a threat to the ideal of a more egalitarian Chinese society.

Digital Education had attracted a huge level of consumer interest in educating their children, and the Chinese changes are intended did to curtail profit taking from such activities. This has erased large sums in the value of these Chinese tech enterprises that are active in the online Chinese education market.

At the same time China is taking steps to stop data leakage and direct data export from China, attempting to curtail the export of Chinese data. This was evident with the float of DiDi on the US market in June of this year, a move that appeared to raise the suspicions that the resulting multinational enterprise would have no qualms about taking a multinational view of their gathered profile data as well. The Cyberspace Administration of China ordered app stores to remove the DiDi app, after citing violations on the company’s collection and usage of personal information. As a result, DiDi stopped registering new users and agreed that it would make changes to comply with rules and protect users’ rights. The Chinese regulators then announced that it would tighten rules for Chinese companies seeking to list or sell shares outside the country. In August the U.S. Securities and Exchange Commission temporarily halted all IPOs from Chinese companies due to the regulatory uncertainty surrounding DiDi and other Chinese companies listed in the US.

Part of the concerns here relate to a domestic Chinese economy which is still highly debt leveraged with few controls and few well-established regulatory levers. The Chinese tech giants were in effect working with an apparent free rein to innovate with consumers on various forms of digital transactions and currencies which cumulatively threatened to create a significant overhang of control across the Chinese economy and potential exercise significant social influence.

The ground beneath Chinese digital enterprises has been well and truly shaken by these government actions. This action also raises the question of foreign investment in Chinese enterprises. China is still reliant on foreign investments, despite the size of its domestic economy. These apparently arbitrary interventions increase the nervousness of foreign investors, which, in turn, puts pressure on the Chinese economy to lift interest rates to factor in this investment risk. The markets in China are highly volatile as a result and this may limit economic growth potential in the near-term future.

The strains in China are similar to those in other parts of the world. How much data can you collect about consumers without their explicit knowledge or consent? What can you do with this data? What controls should you be bound to in storing, using, and on-selling this data? How can the public sector place a rein on the social powers of these new enterprises without scaring off the private sector investment that underpins these enterprises?

Is it going to be “This Time, for Sure!” Or should we expect a Next Time?

I am hard pressed to conclude that these various legislative actions or direct leadership responses will constitute the final word in trying to strike a workable balance between these new business models, driven by various forms of enthusiastically deployed digital surveillance infrastructure, and the desires of national public sectors in trying to seek a sustainable market structure and a stable societal framework.

The aim of these digital enterprises is basically disruptive in nature at the start and as they mature then they naturally change. The emerging model starts to look more and more like a rerun of a colonial model of exploitation where a multinational digital enterprise operates within each domestic economy using a largely extractive and highly exploitative business model that expatriates profits and performs as little in the way of local investment as possible. So, it’s useful to ask what do we mean if we want to open up this extractive and exploitative business model to competition? Adding more operators of the same basic extractive exploitative digital business model hardly seems to represent a desirable outcome. In this case more is probably not better!

My sense is that the unease is not specifically an unease with Facebook, Amazon or any of these other digital giants. It’s not specifically these particular actors per se. It’s not that if some other social network platform had gained the momentum to obtain an effective dominance of this space, then then the outcome would’ve been any different. Anyone else who happened to be in the right position at the right time would’ve created much the same outcome that we have today.

It’s not even the fact that they have established massive Internet-wide functional monopolies or cartels in their respective areas of activity. Even that, as bad as it has become today, is not the major problem we appear to have. Yes, it’s a problem, and the monopoly will naturally exert a repressive force for further innovation and instead it will attempt to divert the collective effort to a more contained level of non-disruptive refinement that does not threaten the incumbency of the established monopoly. But we should remember that monopolies only exist for a moment in time, and their very presence creates a continuing onslaught of competitive pressure which ultimately disrupts their monopoly. Apple and the others will doubtless suffer the same fate as the British East India Company in the fullness of time. In the same way that the telco sector simply could not react with the necessary speed and agility to respond to the Internet in any meaningful way and their very size became a liability, as similar fate awaits all these current digital behemoths. Doubtless these entities will still exist in some way, and they may still be influential for many years to come, in the same way as J. P. Morgan or General Electric are still large and influential corporate entities more than 120 years after their corporate debut, but like these Guilded Age giants, their overarching market powers will dissipate over time under the relentless pressure of competitive forces.

The unease I have about this situation is more of an unease about the fundamental changes to our society as we head down this digital path. There is an increasing appreciation that social networks have undermined our collective trust in some vital public processes (such as elections, for example). There is the sense that there are few, if any, broadly trusted information sources left in today’s world. It appears that the wisdom of crowds is nothing more than a contradiction. There is the sense that we are being collectively challenged with ever larger and ever more significant common problems, but our societal cohesion and collective ability to harness our resources and focus our efforts to address these issues has been significantly eroded.

It strikes me that in attempting to regulate against the overwhelming current market position of these giants we are being distracted by the symptoms rather than looking at the root causes. In the same way that the Sherman Act was more of a reaction to the massive changes in US society that was being wrought as a consequence of the changes from a primary producing largely agrarian society into an industrial society with its associated massive displacement of people, occupations and wealth, we are seeing a similar displacement happen today and a similar reaction from the legislators to this sense of societal dislocation taking place in this digital age. I suspect that in Europe there is an additional irritant in this situation, as the former imperial powers with their respective colonial empires have now joined the ranks of the digitally exploited. The threat of these significant financial penalties will likely offer little in the way of lasting comfort, let alone alter the inevitability of the outcome.

So, yes, we can expect further rounds in this engagement between legislators and national regimes and these digital giants, but I suspect that future rounds will need to change their intended focus and move forward along a path of reconciling our societies to the imperatives of this digital economy. We need to stop applying some basically cosmetic refinements of the regulatory measures of the 1890’s to the world of 2030, and work on the harder problem of coming to terms with what we are doing to ourselves in this digital age. It’s not easy and it will take time, as well as entailing numerous iterations of various public sector responses as we feel our way along this previously untrodden path.